Mortgage Guide

A mortgage is simply the name given to a specialist type of loan used to purchase a property. Commercial and residential properties in the UK can be purchased by taking out one of several different types of mortgages, which in most instances have relatively similar mechanics. Getting to grips with how mortgages work is essential for anyone considering a property investment of any kind. Even then, the importance of seeking independent broker support to ensure you find the best possible deal cannot be overstated. In this guide, we will be taking a look at the most important characteristics and criteria that must be considered, prior to submitting a mortgage application in the UK.

How Do Mortgages Work in Britain?

Mortgages are financial products issued specifically for the purpose of buying properties. They are offered in the form of secured loans, where the property itself is used as security (aka collateral) for the loan. This differs from a personal loan (aka unsecured loan), where no security is required to access the facility. All mortgages in the UK require an initial deposit (or down payment), calculated as a percentage of the property’s market value. The remaining balance of the mortgage is then repaid on a monthly basis, over the course of anything from five to 35 years.

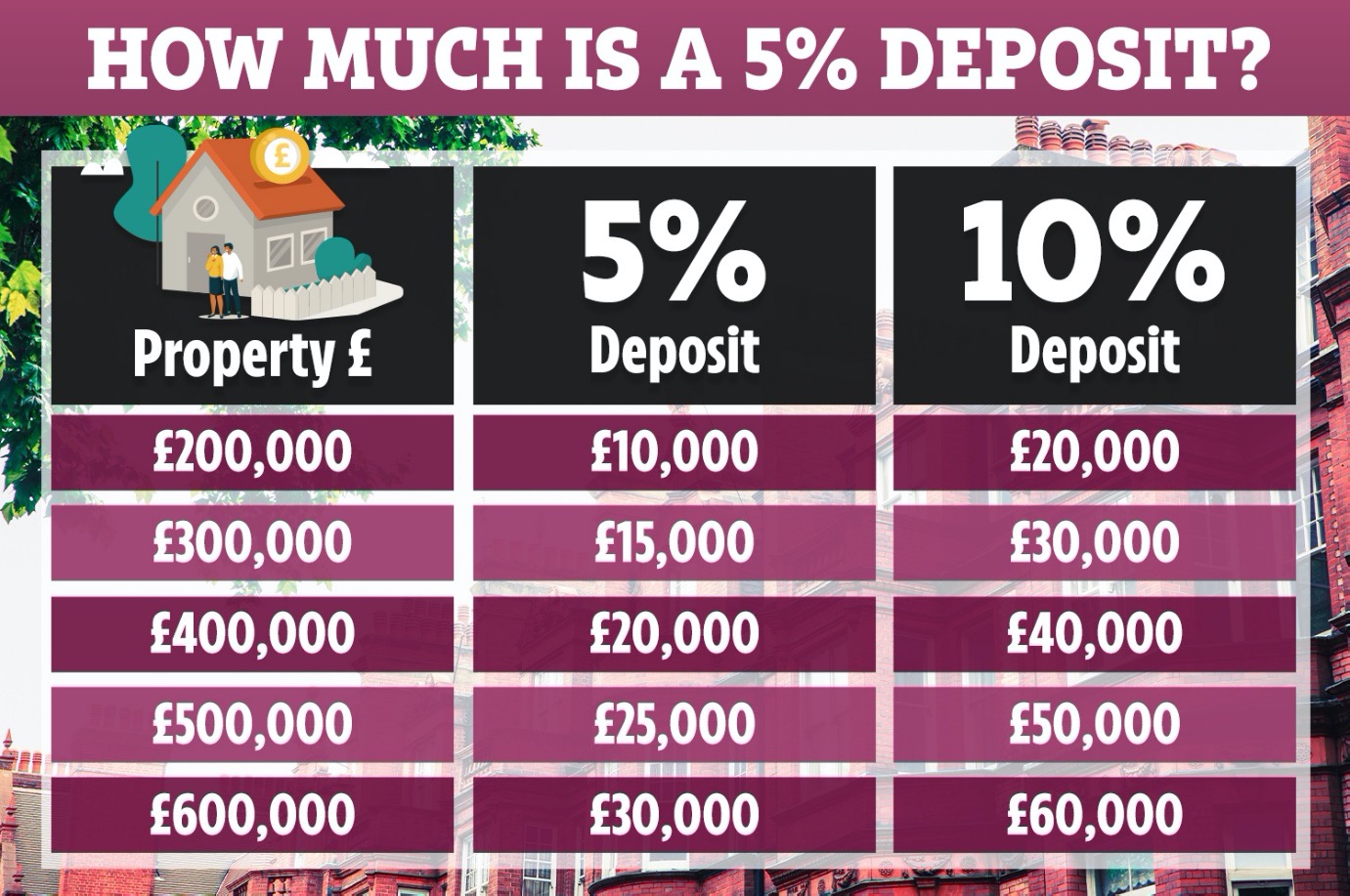

How Much Deposit Will I Need?

Deposit requirements vary significantly from one lender to the next. First-time buyers are usually expected to pay a deposit of 10%, while those looking to relocate or purchase a second property may need to come up with 20%. Buy-to-let investors may need to offer up to 30% as a down payment, though there are some specialist BTL mortgages with lower deposit requirements. The UK government recently introduced an initiative to encourage lenders to offer mortgages with a deposit requirement of just 5%, which may or may not be temporary in nature.

Source: The Sun

What Are the Main Types of Mortgages?

The advice of an independent broker is likely to prove invaluable when choosing from the different types of mortgages available. Most home loans work in a similar way, but there are variations in interest rates, repayment options and incentives offered by lenders.

• Interest Only vs Repayment Mortgage

o Most mortgages are issued as repayment mortgages, where the total balance of the loan plus all interest and borrowing costs is gradually repaid each month over the course of several years.

o With an interest only mortgage, you only repay the interest and borrowing costs of the loan with your monthly repayments. After which, the full outstanding loan amount must be paid in full.

• Fixed Rate vs Variable Rate Mortgage

o A fixed rate mortgage is issued with the guarantee of a specific rate of interest for an introductory period (usually two to five years), after which it is switched to a standard variable rate loan.

o Variable rate mortgages have interest rates that can increase or decrease at any time, typically in accordance with Bank of England base rate fluctuations and the in-house policies of the lender.

• Special Incentive Mortgages

o Another mortgage option to consider are cash-back mortgage deals, which offer cash ‘rewards’ either annually or when the mortgage balance is repaid. Specialist self-build mortgages are also available from many UK lenders at competitive rates.

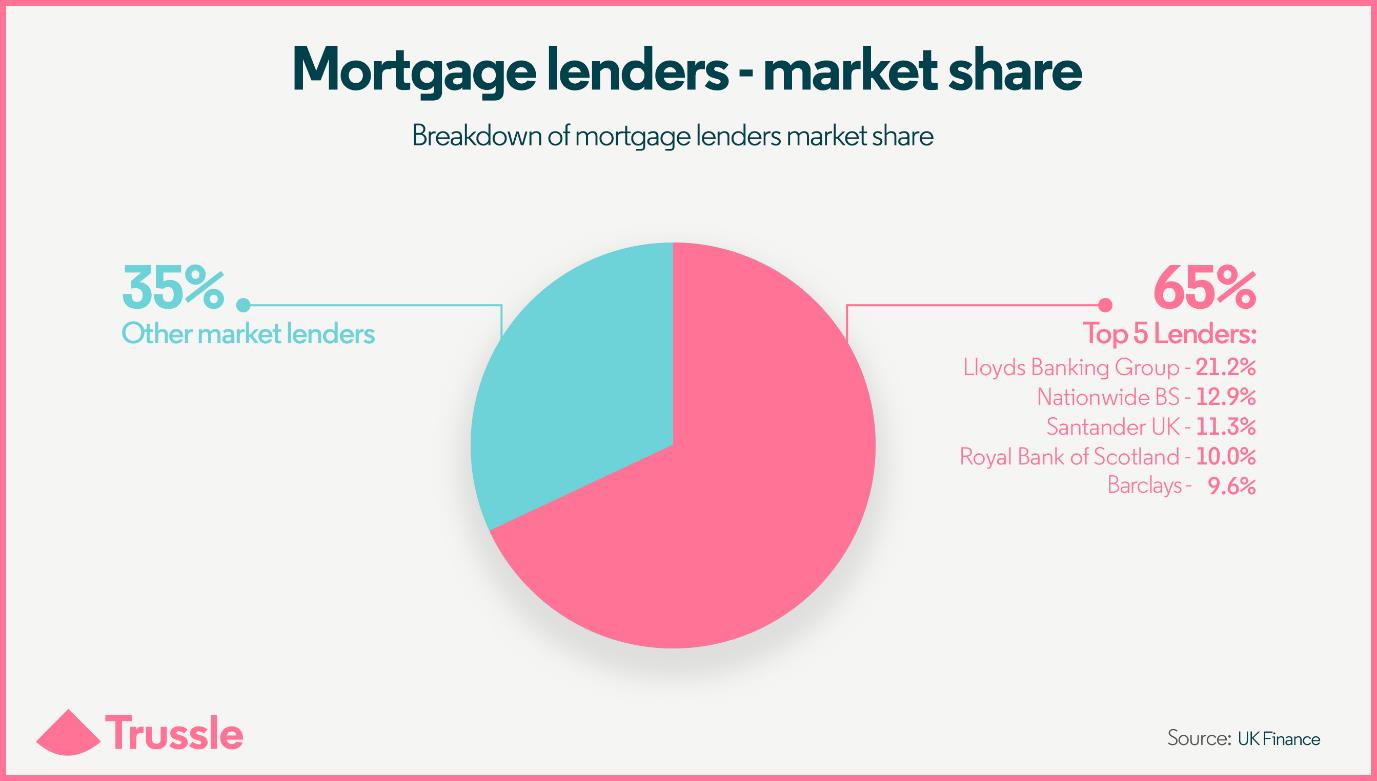

Where Can I Get a Mortgage?

It is estimated that there are currently 100+ banks and lenders in the UK offering a wide variety of mortgage products. Rather than applying directly with a lender, it is advisable to seek independent broker support and arrange an in-depth market comparison.

Source: UK Finance

Some of the most competitive deals on the UK market are not available on the High Street, but can instead be accessed exclusively via an approved broker.

How Much Can I Borrow?

Policies on maximum loan amounts vary from one lender to the next, but there are several primary factors that will influence how much you can borrow, including:

• How much you earn (or your combined annual income for a joint application)

• Whether you already own a home or are a first-time buyer

• The market value of the property you intend to purchase and its condition

• Your outstanding debts including credit card balances, personal loans etc.

• General financial commitments including childcare costs

• Your credit history at the time of your application

• The age and employment status of the main applicant

The size of the down payment you are able to provide may also influence how much you can borrow.

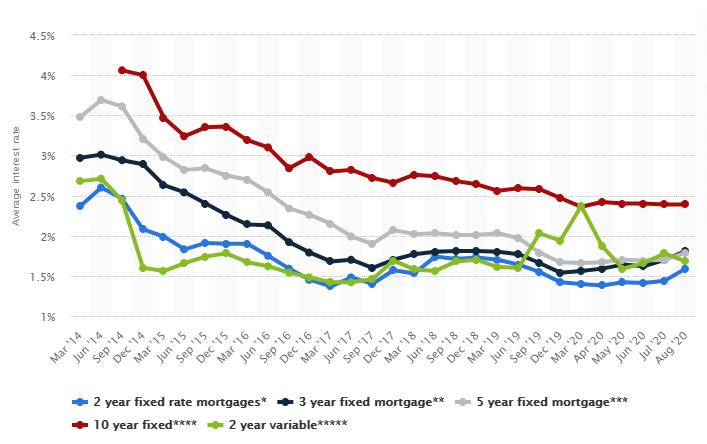

How Much Does a Mortgage Cost?

Source: Statista

Mortgage costs vary wildly from one product, applicant and lender to the next, in accordance with a long list of factors. The most influential of which are as follows:

• The size of the loan - larger loans inherently means higher overall borrowing costs

• Your financial position - high-risk applicants can expect more expensive loans

• Repayment period - mortgages repaid faster are usually more cost-effective

• The APR on the loan - the annual rate of interest the bank or lender charges

• Mortgage type - repayment mortgages are usually more expensive than interest only

• Deposit size - the bigger the deposit, the lower the subsequent borrowing costs

• Insurance costs - applicable if taking out life insurance is mandatory

• Additional fees - variable between lenders (always compare the market in full)

An online mortgage calculator can be a great way of establishing the affordability of a mortgage.

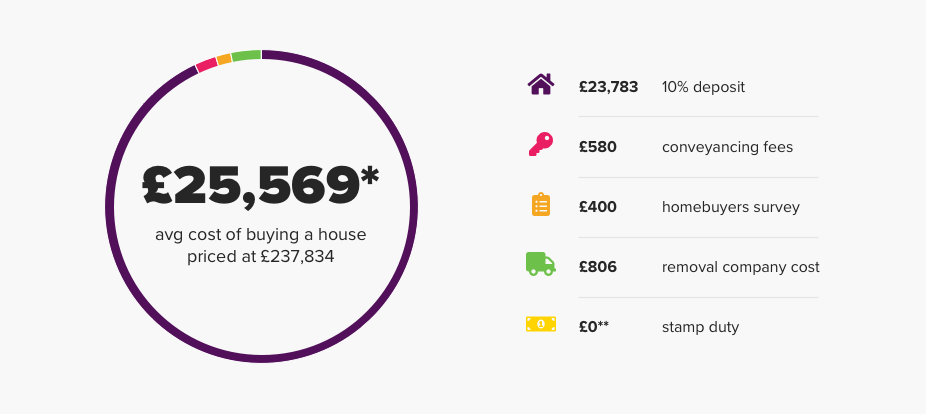

What Fees Will I Have to Pay?

Source: Compare My Move

The annual percentage rate (APR) payable on your mortgage will constitute the biggest borrowing cost of all. However, additional fees and commissions (often totalling anything from 2% to 5% of the loan amount) may be payable, through a combination of the following:

• Stamp duty if the value of the property surpasses the stated threshold

• Legal fees to cover the services provided by solicitors

• Valuation fees and survey fees for the services of contractors

• An arrangement fee for the loan, charged by some lenders but not all

• Early exit fees if you decide to repay your mortgage early

Mortgage broker fees should never be payable by the applicant/borrower, but instead collected from the lender at the time the mortgage is issued.

How Do I Apply for a Mortgage?

The best way to apply for a mortgage is with the help and support of an independent broker, who can help you find a competitive deal to suit your requirements and your budget. It is also essential to establish ahead of time whether your credit history and financial circumstances may exclude you from certain types of mortgages, in order to direct your applications at appropriate providers.

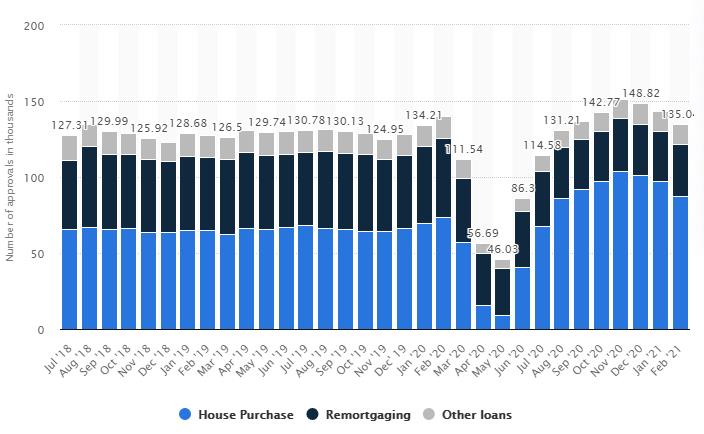

What is a Decision in Principle?

A Decision in Principle (DIP) - aka Agreement in Principle (AIP) or mortgage promise - is a statement issued by a lender to confirm that they are willing to lend you a specific sum of money, based on information provided. However, it is important to note that it is not a legally-binding agreement or a formal contract - the lender can still refuse to issue the mortgage, if they believe it is necessary to do so. Total number of mortgage approvals in the United Kingdom (UK) from July 2018 to February 2021, by loan type:

Source: Statista

What Happens After I Get a Decision in Principle?

Once you have received a mortgage promise from the lender, you can begin the five-step process of finding, buying and moving into your new home:

Step 1. Search for a property

If you have not already set your sights on your dream home, now is the time to find a property you can afford. You will need to base your decision on both the amount of money the lender is willing to offer you and the size of the deposit you are able to provide.

Step 2. Make an offer

Once the property has been inspected and you have decided you would like to buy it, you can make an offer based on its asking price and market value. Your solicitor, estate agent or representative may be able to help negotiate a more competitive price.

Step 3. Get a formal offer

The seller will subsequently provide you with a formal offer to purchase the property, when a final price has been agreed on. You are still able to walk away at this stage if you choose to do so, with no obligation to go any further.

Step 4. Exchange contracts

At this point, you will be required to pay the agreed deposit for the property and sign a legally-binding agreement, confirming your intent to buy it. If you back out of the purchase at this stage, you will forfeit your deposit in its entirety.

Step 5. Transfer of mortgage funds

Your bank and/or legal representative will then organise the transfer of the outstanding balance to the seller, at which point ownership will be transferred to you and you can move into your new home.

What is a Subprime Mortgage?

The term ‘subprime’ is used in reference to a variety of specialist home loans for applicants who may not meet the typical lending criteria of most banks. Typical examples of subprime mortgages include loans for applicants with a low credit score, applicants with no credit history whatsoever, self-employed applicants, applicants with no proof of income and applicants with a history of bankruptcy or insolvency. Competitive deals for subprime applicants are available from a variety of specialist lenders, though most major High Street banks do not issue subprime mortgages of any kind.

What Insurance Will I Need?

Insurance requirements vary in accordance with the lender, the type of mortgage being taken out and the individual circumstances of the applicant. Buildings insurance, mortgage protection insurance and life insurance may be mandatory with some applications - something to discuss with your broker and factor into your affordability checks.

Is There the Option to Switch Mortgages?

It is always possible to switch to a new mortgage, if you become dissatisfied with the competitiveness of your loan or the service provided by your lender. You can switch to a different product with the same lender, or remortgage your home with an entirely new loan from a different lender. However, early repayment fees and penalties may apply when switching to a different mortgage provider. Though it is possible that the savings you would made by switching will augment these fees by a significant margin. If you are interested in switching to a new mortgage deal or lender, consult with an independent broker to ensure you get a good deal.

Some lenders encourage mortgage customers to overpay where possible and clear their loan balances early. Elsewhere, overpayment is penalised with additional fees and elevated interest rates. This is something that must be taken into account before entering into a mortgage contract, if you have any intention of overpaying and clearing your balance earlier than agreed.

Further FAQs:

Is a mortgage right for me?

A mortgage is the only realistic option for most people looking to get on the property ladder. However, not everyone can afford to own their own home, therefore mortgages are not right for everyone. Your broker will help you determine whether or not you can comfortably afford to take out a mortgage.

What if I can’t come up with a deposit?

There is currently no possibility of taking out a mortgage in the UK without offering a down payment on the property. However, deposit requirements vary from just 5% to as much as 40% - depending on the lender you approach and your general financial situation.

What about offset mortgages?

An offset mortgage is worth considering if you have plenty of savings, which can be used to reduce the overall borrowing costs on your home loan. Ask your broker whether your financial circumstances could qualify you for a competitive offset mortgage deal where available.

What additional fees do I ned to know about?

The list of additional fees and commissions payable varies from one mortgage to the next, with chargeable services including:

• Mortgage arrangement fees

• Valuation fees

• Property survey fees

• General transaction fees

• Administration fees

• Fees for missed or late payments

• Consultation fees

• Mortgage broker fees

• Completion fees

• Early repayment fees

All of the above must be factored into your initial affordability checks, though can be minimised by comparing the market in full with the help of a broker.

How do I compare mortgages to find the best deal?

On online comparison site can be a good place to start, but there is an extensive network of specialist lenders who operate exclusively via approved brokers. It is therefore essential to compare the market with the help of an independent broker, who can help you find the best possible deal to suit your requirements and your financial circumstances.

Why Should I use a mortgage broker?

Along with helping you find the best possible deal and saving you a small fortune in borrowing costs, a mortgage broker can streamline, simplify and speed up the process of finding your ideal home alone.

Is there any extra help for first-time buyers?

There are currently several initiatives up and running in the UK for first-time buyers in need of help getting on the property ladder. Examples of which include the following: • Help to Buy

• Help to Buy ISA (now closed to new applicants)

• Shared ownership

• First Steps London

• Starter Homes scheme

The government also introduced a temporary stamp duty holiday in 2020 (now extended to September 30), excluding all first-time buyers from stamp duty liability when purchasing properties valued at less than £500,000.

What about buy-to-let mortgages?

A buy-to-let mortgage works in a similar way to a residential mortgage, though will typically require a much larger down payment - often 30% or 40%. Eligibility for a BTL mortgage is based on similar range of affordability checks, along with the rental income the property is likely to generate, its condition at the time of the application and the track-record of the landlord applying for the loan.

What happens if I cannot repay my mortgage?

Lenders will always do what they can to reach amicable agreements with borrowers, if they run into financial difficulties. Repossession of homes to recoup losses in the event of non-repayment is usually a last-resort option, which will not be considered unless all others have been exhausted. However, your lender will have the legal right to take possession of your home if you are unable to keep up with your mortgage repayments. Mortgage insurance will cover you against certain inevitable eventualities, though is by no means a comprehensive fail safe against repossession.

Is paying off a mortgage early a good idea?

In most instances, overpaying (even on a modest level) each month could lead to major savings on the overall balance of your loan. However, some lenders charge additional fees for overpayment and early mortgage repayment, which should be considered before signing your mortgage agreement.